Persistent low oil prices led to 10 energy companies with a cumulative turnover of EUR8.5bn filing for bankruptcy in the US in 2015 and 6 others (cumulative EUR3.4bn) ended up in a similar situation in Canada.

Chinese state support for capital intensive sectors is fading away in favour of SMEs and high-tech research and development, as well as other high-end activities.

China’s steel industry is particularly affected – overcapacity pressure – the largest insolvency worldwide in 2015 with Sino steel, worth EUR26bn, gone bankrupt in October 2015.

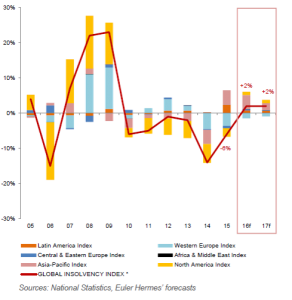

Insolvencies are projected to increase by +2% worldwide in 2016, and by +2% in 2017. Too-low-for-too-long growth, turbulence in some sectors (commodities) and the domino effect of major bankruptcies. In 2015 152 top bankruptcies by companies with sales >EUR100m vs 95 in 2014.

In 2016, Asia Pacific (+13% than in 2015) and Latin America (+17%) are the hot spots. In the U.S., bankruptcies should increase by +3%. This major shift is driven by the Metal and Energy sectors (half all all).

Western Europe is the only region where insolvencies are expected to decrease: -5% in 2016, and -3% in 2017. However, remains higher than pre-crisis levels in 11 out of 17 European countries.

Increasing nonpayment risk in emerging markets is having a toll on exporters.